The Paradox of Prosperity: Why the Worry, and What Comes Next

By Brandon Wester, CFA®, Chief Investment Officer

Over the past three years, markets have delivered some of their best returns in recent memory. Yet many investors spent that same period feeling anxious. Clients kept asking, "Should I be worried?" or "Should we make a change?" That gap between strong performance and lingering unease is exactly what we want to explore in this newsletter.

We will look at what the markets did from 2023 through 2025, and lay out the principles that continue to guide how we manage your investments.

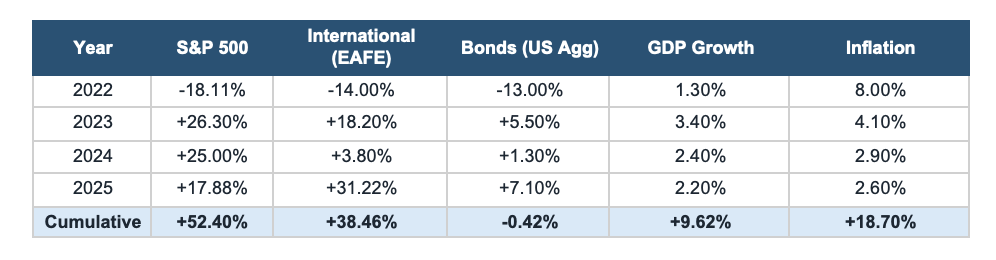

How the Markets Performed

The numbers tell a compelling story. After a rough 2022 across stocks and bonds alike, the market staged a strong recovery and kept going.

Sources: SlickCharts (S&P 500), MSCI, Bloomberg, Trading Economics, Minneapolis Fed

U.S. Stocks: The S&P 500 gained roughly 86% in total over the three-year recovery, well above its historical average. Growth was initially led by tech, but by 2025, many other sectors were pulling their weight too.

International Stocks: Developed markets outside the U.S. also had a strong run. 2025 was especially notable, with international stocks outpacing the U.S. that year. They still trade at lower valuations than U.S. stocks, which may set them up well going forward.

Bonds: After a painful 2022 (down 13%), bonds recovered steadily. With yields now at decade-plus highs, bonds are earning real income again and doing their job of steadying a portfolio.

The Economy: GDP growth stayed positive and beat expectations every year. Inflation came down from 8% to roughly 2.4%, close to the long-term target. Unemployment stayed low, and wages stayed ahead of inflation. The "soft landing" that many said was impossible actually happened.

So, Why Did Everyone Still Feel Worried?

Even with strong returns, the mood among investors never quite matched the market's performance. The headlines were relentless: political turmoil, tariffs, the war in Ukraine, U.S.-China tensions, the Middle East, and a regional banking scare in 2023 when Silicon Valley Bank collapsed. Every one of those events caused short-term volatility. While all those things certainly affected people’s mood, none of them derailed a diversified portfolio over the long run.

This is a pattern worth naming. Headlines about risk often come at exactly the moments when staying invested matters most. Investors who stuck to their plan and resisted the urge to react captured all of those gains. Those who stepped out, even briefly, often missed the strongest days.

Key Lesson: Short-term headlines and long-term market results are often disconnected. Disciplined investors who stayed the course were rewarded.

What We Are Watching Now

Economically speaking, a few concerns are worth taking seriously today, even as the overall picture remains solid.

Technology valuations are elevated. Certain AI-driven companies are priced at levels that echo past peaks. That does not mean a crash is coming, but it does suggest that future returns from those specific names may be more modest. There is an important distinction between high prices built on real earnings growth and pure speculation. We are mostly in the former, but we are watching closely.

Market concentration is real. A small number of large companies have driven a big share of gains. This is not without historical precedent, but it is a risk. Owning a diversified portfolio, including international stocks, small-cap companies, value-oriented sectors like financials and healthcare, provides a cushion when leadership rotates.

Economic growth may slow from here. Fiscal stimulus is fading, and AI-driven efficiency is reshaping some industries. On the other side of the ledger, recent tax policy is a tailwind, and consumer and corporate balance sheets are in strong shape. Banks are far healthier than they were before 2008. Growth moderating is not the same as a recession, and a slowdown in the economy does not automatically mean bad news for markets.

Another risk to the economy is that a large swath of consumers may be falling behind, with the cost of everyday living going up. Over time, this could impact overall consumption and national economic health. While this may become a problem down the road, it does not seem to be negatively impacting the overall economy today.

Our Approach: We are not abandoning growth areas, but we are making sure portfolios are diversified across asset types and geographies. This is not about timing the market. It is about being positioned to hold up across a range of scenarios.

What to Take Away From All This

The markets have rewarded the steady investor greatly over the last three years, far above the historical average. We should view this rally that has given us a healthy lead going into the next three years with appreciation that we captured it. Worrying of a crash because of good results often results in bad outcomes. Yet, having more tempered expectations for the assets that performed the best while knowing there is a world of opportunity is the prudent view.

Diversification is doing its job right now. As of late February 2026, if you had been invested only in large U.S. stocks, your returns would be nearly flat for the year. Broad exposure to bonds and international markets is making a real difference last year and in this one.

Headlines are often inversely correlated with returns. Uncertainty tends to create opportunities for investors who stay patient. Political and geopolitical events feel enormous in the moment and rarely alter long-term market outcomes.

High valuations in one area of the market are a signal to set realistic expectations there, not a reason to abandon your plan. The biggest risk is not market volatility. It is abandoning a well-built strategy at the wrong moment.

Looking Ahead

Risks remain: valuations in certain segments are stretched, and the path of fiscal and monetary policy is not entirely clear. But the foundations are strong. Corporate innovation is robust, global growth continues, and the compounding effect of staying invested over time is powerful.

At Longwave, we know our clients grapple with these mixed messages all the time: markets are up, but so is economic pressure. As a nation, prosperity is also not evenly distributed. When it comes to financial advice and investment management, however, our role is to create the best outcomes for our clients, and that most often means focusing on long-term goals rather than short-term fears.

Thank you for your continued trust. We look forward to finding the world of opportunities in the year ahead with you.

Sources:

S&P 500: Slickcharts

MSCI EAFE: MSCI

US Agg Bonds: UpMyInterest

GDP: Trading Economics

Inflation: Federal Reserve Bank of Minneapolis / US Inflation Calculator

This material is intended for informational/educational purposes only and should not be construed as investment advice, a solicitation, or a recommendation to buy or sell any security or investment product. Please contact your financial professional for more information specific to your situation. All indices are unmanaged, and investors cannot actually invest directly into an index. Unlike investments, indices do not incur management fees, charges, or expenses. The main risks of international investing are currency fluctuations, differences in accounting methods; foreign taxation; economic, political, or financial instability; lack of timely or reliable information; and unfavorable political or legal developments. Diversification does not assure a profit or protect against loss in declining markets, and diversification cannot guarantee that any objective or goal will be achieved. Investments are subject to risk, including the loss of principal. Some investments are not suitable for all investors, and there is no guarantee that any investing goal will be met. Past performance is no guarantee of future results.