Short-Term Turbulence, Long-Term Stability: Our Thoughts on Iran, Oil & Markets

What do recent geopolitical developments mean for your portfolio, and why staying the course is the right move.

A NOTE ON CLIENT STEADINESS

We want to start by acknowledging something we have genuinely appreciated: the measured, steady approach our clients have taken over the past month. As geopolitical tensions in the Middle East have escalated your relative calm has been encouraging. Staying committed to a long-term plan during uncertain periods is harder than it looks, but it tends to serve investors well.

Investors who make significant portfolio changes by chasing headlines have often found, in hindsight, that patience (or blinders) would have served them better. We are grateful for the trust you have placed in us and want to offer some context on what we are watching for right now.

WHAT IS HAPPENING

The U.S.-Israel military campaign targeting Iran has sent energy prices soaring, with Brent crude exceeding $100 a barrel. Headlines are understandably focused on the disruption, but it is worth keeping perspective on what this situation likely means over a longer time horizon.

The temptation is to see today’s conflict as “unprecedented”, but the Gulf region has been a source of geopolitical and economic instability for at least half a century. Indeed, over that time, there have been multiple occasions of energy price volatility – up and down. Today, while the US is in a unique position of having meaningful energy independence, we live in an interconnected world. What happens overseas affects our pockets and our portfolios.

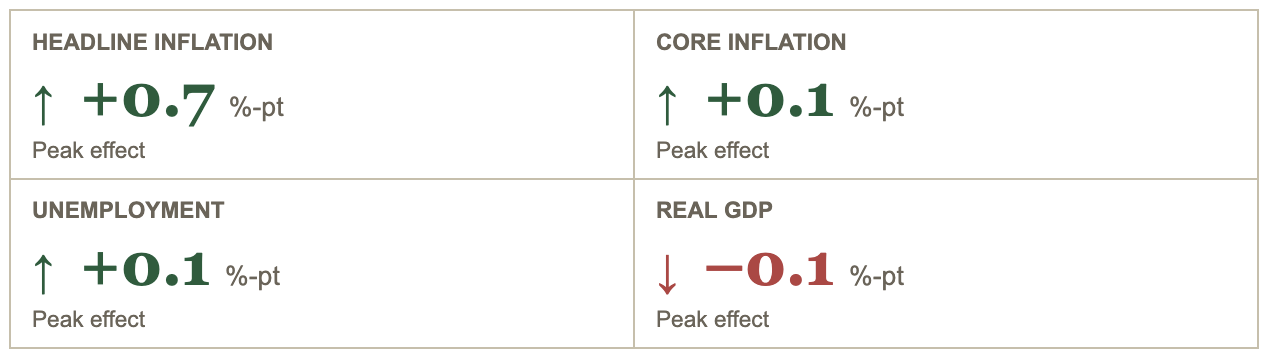

For the US, the impact of $100 oil would be visible but modest:

Estimated Peak Economic Impact: $100 Oil

Fed model estimates show modest macroeconomic drag from a persistent shock to oil prices

Source: Apollo Global Management / Federal Reserve model estimates

On the other hand, the impact on overseas economies (not to mention Gulf countries on the front lines) has been more significant. With oil and gas prices increasing by 50-100%, there has been real inflationary pressure on everything from food and agriculture to transportation and manufacturing. For instance, much of the world’s helium, necessary for various industrial applications, comes from Qatar. This has real negative consequences on consumers’ purchasing power, global economic activity and national budgets.

RATES: HIGHER FOR LONGER

Another practical consequence worth watching is what this means for interest rates. With core inflation already sitting above the Fed's 2% target, an oil-driven bump in headline inflation makes it less likely that the Fed will cut interest rates. The majority of FOMC members have already signaled comfort with holding rates steady, and oil remaining above $100 reinforces that view.

What this means in the short term:

CONTEXT

The near-term disruption from higher oil prices is real but temporary. Once geopolitical uncertainty fades, the expectation is that rate cut expectations will return and long rates will move lower, bringing relief to rate-sensitive areas of the economy.

OUR VIEW & YOUR PORTFOLIO

According to pundits, there are all kinds of portfolio adjustments that can be made to deal with this conflict and the risks it brings. However, with much of the bad news already priced in, it’s probably already too late for major portfolio changes. If an investor made such a move now, they would have to reverse course at some later date…. but when!? They would probably miss the bottom as well, thus losing on the way up and on the way down.

A more measured approach would be accepting the historical precedent that this conflict and its economic impact are likely temporary. No country wants endless war, and already we are seeing overtures of peace. While the path towards Middle East stabilization remains murky, at some point, the geopolitical situation will stabilize. When that happens, the inflationary impact from higher oil prices should fade, and things should return to a more normal economic path.

At Longwave, we feel good about your portfolio as currently constructed: a tilt towards value that avoids the frothiest parts of the market, diversification that aims to blunt volatility, and a bond mix that has done a good job of balancing income with stability. If you are drawing distributions from your investments, the stable parts of your portfolio can reliably generate income for years to come. Longwave’s approach behind your portfolio was built to absorb this kind of short-term shock, and we view this as a temporary period of disruption amidst longer-term structural growth, productivity gains and innovation.

KEY TAKEAWAY FOR CLIENTS

Short-term volatility is inevitable along the journey to long-term returns. Geopolitical shocks are real, but they also tend to be temporary. Shifting strategy based on headlines has historically been one of the more reliable ways to underperform. Staying invested and avoiding a “this time is different” mindset, has generally produced the best results.

We are monitoring developments closely and will be in touch with any material updates. If you would like to talk through any of this, please do not hesitate to reach out.

This newsletter is for informational purposes only and does not constitute investment advice. Past performance is not indicative of future results.

This material is intended for informational/educational purposes only and should not be construed as investment advice, a solicitation, or a recommendation to buy or sell any security or investment product. Please contact your financial professional for more information specific to your situation. All indices are unmanaged, and investors cannot actually invest directly into an index. Unlike investments, indices do not incur management fees, charges, or expenses. The main risks of international investing are currency fluctuations, differences in accounting methods; foreign taxation; economic, political, or financial instability; lack of timely or reliable information; and unfavorable political or legal developments. Diversification does not assure a profit or protect against loss in declining markets, and diversification cannot guarantee that any objective or goal will be achieved. Investments are subject to risk, including the loss of principal. Some investments are not suitable for all investors, and there is no guarantee that any investing goal will be met. Past performance is no guarantee of future results. Market data and third-party research referenced herein are sourced from public market sources as of March 2026.